Privcap Preqin Fundraising Roundup, Q2 2016

The second installment of Privcap’s quarterly video series featuring expert insights on the private equity fundraising environment. In this edition, Alan Pardee of Mercury Capital Advisors, Chris Elvin of Preqin, and Privcap CEO David Snow discuss the Q2 fundraising tally, how the large amount of dry powder impacts PE investing, and what effect the crisis in Europe will have on fundraising. Plus, a special guest interview with Bruce C. Greenwald from Columbia Business School.

Transcript Download Transcript

Q2 2016 Fundraising Roundup

David Snow, Privcap: In today’s episode, why it’s a buyer’s market for smaller, newer funds; Dry powder hits a new record, tough sledding for European funds. And highlights from our interview with Professor Bruce Greenwald of Columbia Business School.

Hi, I’m David Snow, CEO of Privcap, and today we are joined by Alan Pardee of Mercury Capital Advisers, and Chris Elvin of Preqin. Gentlemen, welcome to Privcap today. Thanks for being here.

Alan Pardee, Mercury Capital Advisors: Thank you.

Chris Elvin, Preqin: Thank you.

Snow: Okay, first topic. Why is it a buyer’s market now for smaller, newer funds? What do we mean by this? Well, according to Preqin, there are now more than 1,700 private equity funds in the market seeking capital, and a huge amount of these are smaller, newer funds. So, Alan, what’s your take on that?

Pardee: [It’s an interesting market right now. The big mega funds have been getting a lot of the capital, and that’s one of the features of our marketplace.

Snow: Which are on like fund five, six, seven, yeah.

Pardee: Well, exactly.

Snow: [Been going on for a while ?].

Pardee: And because of the fact that most limited partners are a little bit nervous about the state of the world, they’re heading towards the established funds, and that established fund definition can be large, but it can also, luckily for the midsized guys, be midsized or small.

Where the challenge really is right now are around the newer funds. The first time funds. The spinout groups. 2012 to 2014, those guys were very much in favor. Now that the market’s a little more worried, now they’re heading more towards the established firms.

Elvin: You look at the number of funds in market, which you mentioned is over 1,700 now, what’s interesting about that is the actual total aggregate target capital they’re all seeking is actually smaller than at the high point of, say, the end of last year. So there’s an inference there that the smaller funds make up a larger proportion of the new entrants to the market.

Snow: Well, if you are an LP with an appetite for smaller emerging managers, which, by the way, if they do well, tend to outperform the market generally, you probably have an ability to negotiate very good terms for yourself. And so, are you seeing any evidence of that in today’s market that sort of, if you’re a newer fund, you have to make concessions to your anchor LPs?

Pardee: Oh, absolutely. Currently, I would say it’s almost standard practice at this point, that as a newer firm is coming into its first closing, that it’s making some number of concessions to the investors who are joining them in that closing. The typical request is for a discount on management fee. Somebody coming in with 10, 20, 30 percent of the fund, if that is even happening, usually asks for some kind of discount. If it’s 2 percent, maybe they’re getting 1 ½, if it’s some other number, a sizeable discount. The potential for a US fund, to use a US example, taking a European waterfall is also another outcome. We try to keep the European waterfalls over there on the other side of the pond, if we can, but it does happen that they come across.

Snow: Chris, are you seeing anything interesting by way of terms and conditions in today’s market?

Elvin: We’ve recently looked at fund terms and conditions for the pool of data that we have, and we’ve actually this year seen a movement within the hurdle rates of that, that level actually increasing. So I think there’s been a trend in terms of GP and LP alignment, definitely, as Alan says, moving towards the LPs.

Snow: There’s a very well know large private equity firm out there that I believe is based in Boston that, because of the high demand to get into its fund, did away with a hurdle rate, correct? And so, have you seen many other instances of that, or is that an outlier?

Pardee: Oh, I would say there are a lot of instances of high demand funds being able to create their own terms. So there are two different trends to your haves and have-nots out there, including what’s going on in Boston. And others that we can point to both in the US as well as overseas.

Snow: Further to the haves and have-nots theme, your data, or Preqin’s data, shows that, again, the funds that are closing are tending to close at or above their target, and that there are only a minority of funds that are closing or closing beneath the target, which would suggest that, again, those that are successful are successful in spades.

Elvin: Absolutely. And, you know, I think this touches on the point we’ve discussed already. The distributions have happened, the LPs have a lot of liquidity at the moment, and it’s a question of they’re able to funnel that, but where and with whom is really the key decision that they’re making.

Snow: Maybe a final question, and that has to do with a proliferation of groups within the private equity market, and other private funds markets. I guess you could call them seeding organizations. They seed GPs, they will invest in the management company of a firm that is a private equity firm. Is this a result of the difficulties and risks of spinout in emerging groups, and therefore these groups seeking partners or being open to partners coming in and taking a chunk of their firm?

Pardee: Now that the attention has gone to the larger, more established funds, it’s a perfect time for the seeder groups to spend time with these newer managers, these emerging managers, groups that may have spun out from somewhere, and give them a hand. Now, giving them a hand, they’re in the business of doing this, so they create economic outcomes that are attractive for themselves.

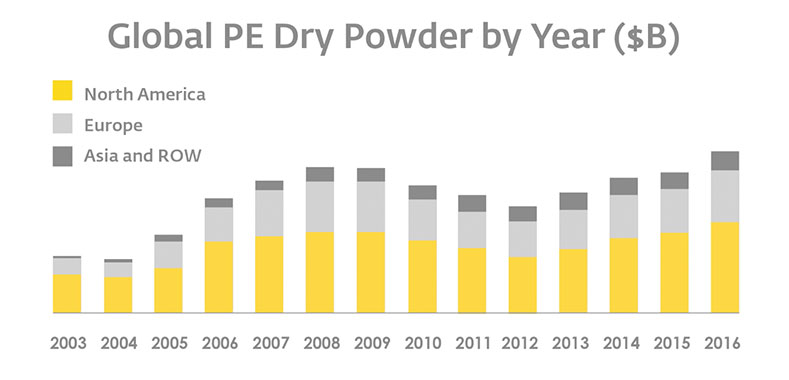

Snow: Okay, next topic. There is more dry powder than ever. So, according to Preqin data, since just the end of last year, the private equity market has added fully $73 billion in un-invested committed capital, sometimes known as dry powder. Chris, what does this indicate?

Elvin: Essentially, I think it goes hand in hand with the growth of the industry. There are more private equity held assets than there’ve ever been before. We’re coming off the back of a robust fundraising period as well. I think there’s more interest in terms of when the pricing, perhaps, will decrease, allowing fund managers to put more of that capital to work. It’s sort of a balance of scales, as it were.

Snow: Alan, a question for you about LPs. Are they focused on dry powder as a metric, or do they have other considerations that they think about first?

Pardee: I think dry powder is really a statistic or metric that is most focused on by the M&A adviser, where they start thinking about the deployment of capital and the deal volume that it needs to meet that for it to come out in the next year, or two or three, whatever the clock might suggest. I think the LP is far more focused on their own budget, their own pacing study, the amount of capital that they have available to deploy into private equity, and what the opportunities are out there. Their first objective is to figure out, with the money that’s in front of me what am I supposed to do with it in the here and now?

Snow: There was an issue that popped up in the market downturn, with LPs not having enough liquidity to fund the capital calls as a result of the predecessor amount of dry powder, right? Can you walk us through that, and why that was a problem?

Pardee: Well, when the pie shrank so dramatically, a certain number of limited partners had fixed allocations. Maybe they were supposed to deploy 10 percent of their overall portfolio into private equity, and they woke up one morning in 2008/9 and found themselves at 30 percent, or 40, whatever the number might’ve been, and a very illiquid asset class, and they had to do some pretty radical measures to try to rebalance themselves. Some of them pursued secondary, some of them did other things to rebalance, but one of the things they did do was they picked up the phone and spoke to the general partners that they had some of this dry powder in their hands, and asked them, please, please, don’t call my capital.

Snow: So what would it take to start reducing this pile of cash, this dry powder?

Elvin: If we start to see a drop in the pricing, entry level pricing, then that in turn, I think, will facilitate them being able to deploy a lot more of this capital.

Pardee: Clearly in Europe we’ve just seen the repricing. Will we see a repricing in the United States? Time will tell. But we certainly feel like we’re closer to the top than the bottom.

Snow: Alan, I’m glad you mentioned Europe, because that takes us to our next topic, which is it’s tough sledding out there for private equity funds, targeting deals in Europe. In the second quarter of 2016, funds targeting Europe raised half as much as funds targeting North America. And here’s a fun fact. European funds raised 33 billion in the second quarter, but 10 billion of that was an Ardian secondaries fund, which, if you take that out, the numbers are even lower. So, Chris, what in general is behind this sluggish fundraising pace for European funds?

Elvin: North America has been the driver behind the fundraising in this particular quarter, and Europe has been slower. Asia and the rest of the world as well, they’ve actually seen more funds close, but less in terms of value. And I think, ultimately, it again comes down to the volatility within the markets.

Snow: Alan, why are North American funds the belles of the ball in the global fundraising market?

Pardee: The North American funds are doing well today because people believe in what’s happening here in the US, and, to a degree, in Canada, in terms of the growth that’s still happening. We are the one economy at the moment that feels like it’s healthy and doesn’t have too extreme risks.

Snow: So an important point is that European LPs remain active, but they’re very active in flowing capital to US or North American private equity funds, and less active in investing locally.

Pardee: I would say they’re still active even in investing locally, but they have the same amount of cautionary look as it relates to what they’re thinking about, if you point towards the United Kingdom.

Snow: I’ll ask a question. You’re based in London. Will the UK private equity industry exist in five years because of Brexit?

Elvin: I think it certainly will. We’ve recently done some surveys both of fund managers and investors, to gauge their interest, and to be honest, there is a mixed bag of results. A very large proportion are simply unsure at this point what they are going to do, until there is a more definite outline of will the UK have access to the single market, won’t they, when will the Article 50 vote actually be exercised?

Pardee: If one is taking a ten-year look at the UK at any moment in time, one has to come to a belief that it’s a growing economy, thriving industries live there, there’s a spirit of innovation that takes place in the UK.

David Snow: Let’s now turn to a highlight from our recent interview with Professor Bruce Greenwald from Columbia Business School.

Michael Ricciardi, Mercury Capital Advisors: So Carl Icahn has said that what’s going on right now is in effect a replication of what took place in 2007, 2008. And in fact, the market is about to go off a cliff.

Bruce Greenwald, Columbia University: Okay, so let’s talk about that in detail. The first thing is that the valuations are actually not as rich as they were in 2007.

Ricciardi: That’s based on PE?

Greenwald: Yeah. The second thing is that the craziness where nobody thought there was any risk so that for example, in 2007, you could by credit default swaps on Dubai sovereign debt, the riskiest region in the world, dependent on the most unstable commodity in the world, which is oil for four basis points, which is once in 2,500 years, they’re going to go completely under. So that craziness is not in the market.

The real issue is the earnings power of these companies so that, if you look at people like Jeremy Grantham, who has been now for nine years, doing the Carl Icahn story. Their view is that these earnings levels are not sustainable. And what you’ve seen is that is a share of total US income, corporate profits, which pre-1990 were about 8.5% are now around 13.5% to 14%. So there’s been this huge increase in profits.

If that increase in profits is sustainable and it’s likely to continue then we may have a flat market for a while. We may not have the kind of increase in prices that we’ve had, but we’re probably not going to see the kind of crash we saw in 2008, 2009.

Now, I think that profits are going to stay where they are and I think that’s the important thing

Snow: Well, that’s it for our program. Thank you to Alan Pardee and Chris Elvin for your expertise, and thank you for watching, and we’ll see you next time.

Sponsors

-

Preqin

Preqin is the alternative assets industry’s leading source of data and intelligence. Our products and services are utilized by more than 40,000 professionals located in over 90 countries for a range of activities including investor relations, fundraising and marketing, and market research. Preqin, founded in 2003, operates from offices in New York, London, Singapore, San…

-

Mercury Capital Advisors

The firm was founded by the former leadership of the Merrill Lynch Private Funds Group, where they received industry-wide accolades as Best Placement Agent in North America, Best Placement Agent in Europe, and Best Placement Agent in Asia. At Mercury, we continue that tradition of excellence. With offices in New York, London, Boston, Dubai, San…

Related Videos

-

Fundraising Roundup – Private Equity 2016 Review & Outlook

2016 in review – LPs allocation challenges, VC boom, fund of funds stagnation.

February 10, 2017More -

Private Equity in 2016 – Dry Powder

A brief overview of the growth of private equity “dry powder” in 2016. Featuring experts from EY and Preqin.

January 22, 2017More -

Fundraising Roundup Q3 2016

The third installment of Privcap’s quarterly video series featuring expert insights on the private equity fundraising environment.

October 17, 2016More -

Columbia’s Bruce Greenwald: Are Corporate Profits Sustainable?

Bruce Greenwald of Columbia Business School talks about the current state of financial markets, the death of U.S. manufacturing, and why the service sector is likely to support today’s historically high corporate profit levels.

July 18, 2016More -

Geopolitics and Real Estate Investing

Michael Fascitelli of Imperial Companies and Michael Ricciardi of Mercury Capital Advisors discuss politics, climate change and other risks.

June 30, 2016More -

Privcap/Preqin Fundraising Roundup, Q1 2016

A new quarterly video series featuring expert analysis of recent fundraising trends and numbers.

April 30, 2016More

Related Articles

-

Powerhouses in PE: Geoff Rehnert

RSM’s Don Lipari sat down with Geoff Rehnert, co-CEO and co-founder of Audax Group, to discuss deal flow and valuations.

July 29, 2016More